eBusiness Weekly

Chris Chenga

Abrupt price increments startling consumers, parallel markets for foreign currency spiking premiums, and in the preceding month to all this, a stock market rally, affirmed investors’ fears on the Zimbabwean Stock Exchange. These occurrences exemplified how an economy can be susceptible to currency and pricing shocks, which inevitably lead to hyperinflation and investment losses.

Thought should be given to how an economy can sustainably position itself to be resolute against such shocks. In Zimbabwe’s case, there is a need for a reliable measure that monitors and controls currency and pricing shocks.

Producer Price Index

There is an economic metric called the Producer Price Index (PPI). Regrettably, Zimbabwe is barren of statistical metrics such the PPI, thus we do not have a formal one. However, understanding PPI and the variables that would go into it, would help clarify our present circumstance.

The PPI ideally provides government, analysts, business managers and private investors with information about the trends in prices at various stages of the production process.

This is helpful for businesses in making capital investment decisions, for analysts in explaining economic trends, investors to determine sound micro-investments, and ultimately, for governments to achieve price stability and control of inflation! Multiple stakeholders have something to gain from the PPI. More importantly, a PPI focuses all these stakeholders within the same context; productivity!

The Producer Price Index (PPI) is a weighted index of prices measured at the producer level. It traces the cost of production for different manufactured goods and commodities produced in an economy.

Of course, the notion is not new in Zimbabwe as a high cost business environment has been identified before. However, by compiling organized data for PPI — which we do not have — it is easier for stakeholders to track the actual means and effort it takes to make an economy safe from currency shocks and price volatility.

Other economies are so precise as to disaggregate the PPI for each sector in the economy. For instance, energy, mining, agriculture, or textiles sectors would all be disaggregated so that a country can trace the prices within each sector, and their contribution to the overall economy. This should not be difficult for Zimbabwe. We are not a broadly diversified economy, so disaggregating sectors should not be so laborious.

Monetary policy is secondary to PPI

The Reserve Bank of Zimbabwe through its monetary policy has received unwarranted blame for last week’s tremors. Some perspectives have misinterpreted the bank’s capacity in controlling currency and pricing stability. Currency shocks, such as the elevated premiums for US dollar, can hardly be the fault of a central bank which has no sovereign printing capacity traceable to PPI.

This is true in the Eurozone which shares the Euro, or any other nation within a currency board. The RBZ is really only accountable to structural stability in the monetary system, for instance easy transactionary platforms for commerce and astute allocation of currency.

For now, John Mangudya can hardly face ridicule in how he has managed the structural stability of our monetary system. But even these structural adjustments of the monetary system are secondary to PPI. The fact is, as long as Zimbabwe’s PPI averages higher than its trade counterparts — irrespective of the amounts of bond notes the RBZ puts into the market — foreign currency reserves will deplete adding to their premiums!

An investor’s eye for PPI

Any asset manager worth their salt would appreciate PPI and its effect on asset prices. Sure, managers could be commended for moving away from liquid assets finding solace in stocks. But erudite managers are aware that the fragilities pervading liquid assets are merely derivatives of weak PPI performance in the economy. As long as Zimbabwe’s PPI averages are higher than trade partners, there will be a burden on the ability of investors to repatriate their returns from stocks for example.

The inevitable currency shortfalls create a circumstance where exchange controls increasingly become more confining; not through any malevolent intent to disadvantage investors, but for the mere sustenance of the economy. It would be incompetent on the asset managers’ part to imagine that the stock market becomes a haven unaffected by PPI. The most competitive and resilient portfolios are likely the ones with the lowest PPI, or at least have greater control of their PPI relative to their sector competitors. It is a hypothesis worth testing on Zimbabwean stocks if data could be accurately compiled. Allow me to use an example in the USA before the financial recession of 2007.

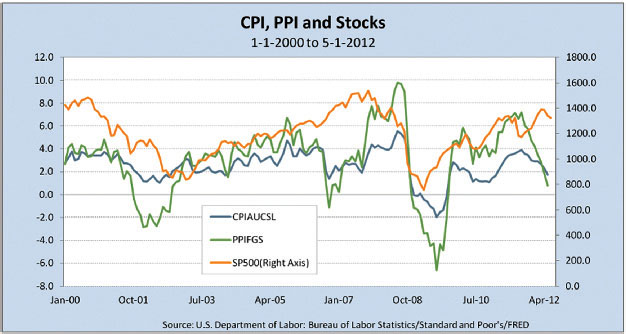

As highlighted by Mike Patton of Forbes magazine in an article titled, “Consumer Prices, Producer Prices and Stock Performance: A Unique Perspective”, since 2001 stock prices (orange line) on the S&P index were going up. But in 2007, when the PPI (green line) rose to an extent that was higher than retail prices CPI (blue line), stock prices fell. Logically as producer prices rise at a much faster rate than consumer prices, it reduces margins and puts pressure on stocks.

Thus, whilst the ZSE may very well be overpriced at the moment, the shrewdest investments would be entities that have some level of control on their PPI, or at least have greater discretion than their sector competitors. This drifts well into a market deficiency of the Zimbabwe economy.

Producers relinquish control of the pricing power

Very few producers in Zimbabwe have pricing control. Indeed, many of them have pricing recommendations that they pass onto their retailers, but due to the scattered retail sector in the economy, that pricing power is weak.

This is what occurred last weekend. Oil producers such as United Refineries, Surface Wilmar, and Pure Oil may have a PPI in the operations, but that PPI was divorced from the pricing that retailers across the country decided to charge for their commodity. Granted there are retail leaders such as TM Pick n Pay, OK and Choppies, but even these retailers cannot claim any pricing power as the sector is open to any individual who can access stock at wholesale, going out to then charge whatever price they wish at their tuck shop, car trunk or homes. This is where all pricing control is lost, and the economy becomes vulnerable to inflation!

Pricing and production interventions

Government interventions should move backwards from what has just been presented. Firstly, the economy must restrain pricing power, not through price controls, but through establishing pricing power to a limited amount of retailers. This is done in developed economies through retail licenses and permits. This deters profiteering and arbitrage opportunities for informal retailers. Of course this would be a politically difficult exercise as many retailers are doing so because they have no alternative occupation, but it must happen.

Secondly, the benefit of an identifiable PPI for every sector is that it enables margin evaluation for licensed and permitted retailers. Because the PPI measures prices at all levels of output for producers, it gives a credible benchmark for what can then be perceived as profiteering, consumer exploitation, and other pricing regulatory standards. This is also how producers like United Refineries in the oil sector can then have structural support to enforce their pricing recommendations to their selected retailers. Inflation, is then manageable and within solid structural monitoring without intervening competitive retail markets.

Thirdly, focus then goes into the PPI at producer level. For instance, by identifying an average sector PPI for 1liter of milk, government can then assess strategies of enhancing economic environment to make that PPI more competitive. It then finds specific metrics that are stressing milk producers.

What Government will find is that fiscal and industrial policies have the greatest impact on whether or not PPI will improve or not in an economy.

Attracting investment into technology, workforce development, infrastructure availability, and other intentional strategies to make Zimbabwe’s PPI conducive for local production become the precise approach.

As our PPI improves relative to trade partners, we then accumulate foreign reserves, secure local and foreign markets, and more importantly, retain price stability to control inflation. These are the right ways to respond to what we just experienced over the last weekend. Indeed they are the correct deterrents to future pricing and currency shocks. These are sustainable resolutions as well.