eBusiness Weekly

Jacob Mutevedzi

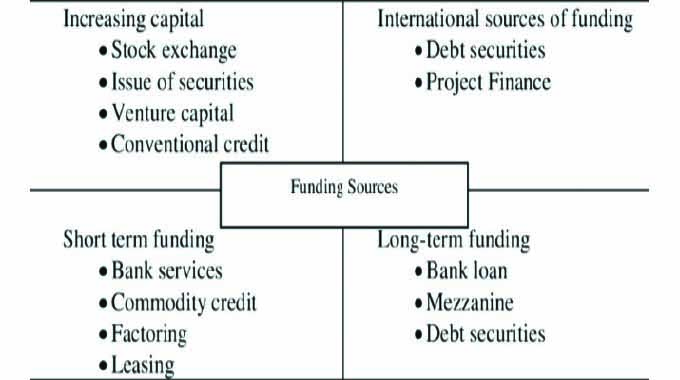

Project finance comes from an assortment of sources. The major sources are equity, debt and government grants. The source of financing has important implications on the project’s overall cost, cash flow, ultimate liability and claims against project income and assets.

Raising finance depends on the nature and structure of the proposed project financing. The interest of investors and lenders will differ depending on the goals and risks related to the financing.

Commercial lenders desire projects that have predictable political and economic risks. Conversely, multilateral institutions are usually less concerned with commercial lending criteria and will look towards projects that ostensibly satisfy not only purely commercial criteria.

Below is a discussion of these manifold sources of project financing.

1. Equity

Equity is usually sourced in the stock markets and from specialised funds. It is more expensive than debt financing. Equity providers require a rate of return target that is higher than the interest rate of debt financing. This is designed to compensate the higher risks assumed by equity investors who wield a junior claim to income and assets of the project.

2. Developmental loan

This is a loan availed during a project’s developmental phase to a sponsor with inadequate resources to execute the project. The developmental lender is usually a lender with notable project experience. Lenders like these, who finance the sponsor during an extremely risky phase of the project, are primarily motivated by equity rewards for the risk assumed.

3. Subordinated loans

Subordinated loans, also called mezzanine financing or quasi-equity, are senior to equity capital but junior to senior debt and secured debt. This type of lending is found between senior bank debt and the equity ownership of a project.

Mezzanine loans take more risk than senior debt because regular repayments of the mezzanine loan are made after those for senior debt.

Subordinated debt has the advantage of being fixed rate, long term, unsecured and may be considered as equity by senior lenders for purposes of computing debt to equity ratios.

4. Senior debt

The senior debt of a project financing often comprises the biggest portion of the financing and is usually the first debt to be placed. Senior debt constitutes debt that is not subordinated to any other liability.

This means it will be the first to be paid out if the project is liquidated. Senior debt falls into two categories: unsecured and secured loans as discussed below:

i) Unsecured loans

These loans depend on the borrower’s general creditworthiness, as opposed to a perfected security arrangement. Frequently, they contain a negative pledge of assets to prohibit the pledge of the company’s valuable assets to third parties ahead of the unsecured lender.

ii) Secured loans

These are loans where the assets securing the loan have value as collateral, which means that such assets are marketable and readily convertible into cash. In a fully secured loan, the value of the collateral is equal to or in excess of the amount borrowed.

5. Syndicated loans

A syndicated loan is availed to the borrower by two or more banks, known as participants and is governed by a single loan agreement.

The loan is arranged and structured by an arranger and managed by an agent. The arranger and the agent may also be participants. Each participant provides a specified percentage of the loan and receives the same percentage of repayments.

6. World Bank sources

The World Bank funds infrastructure development projects all over the globe. While such financial intervention is limited, the involvement of such an institution is beneficial to a project because it provides the much needed credibility necessary to validate the project in the eyes of banks which may be invited to participate in a parallel syndicated loan facility.

Some of the World Bank’s financing programmes are:

i) Loan Programme — The Bank provides loans to member countries to finance specific projects. To qualify, the borrower must demonstrate that it is unable to secure a loan for the project from any other source on reasonable terms.

Therefore, it is invariably considered as the lender of last resort. Moreover, the borrower must prove that the project is technically and economically feasible and that the loan can be repaid.

ii) Guarantee Programme — The World Bank Partial Risk Guarantee Programme provides private sector lenders with limited protection against risks of sovereign non-performance and against certain force majeure risks.

iii) Indirect support — The Bank’s involvement in a project can be pivotal. Even though the financial commitment is negligible, World Bank involvement confirms that the loan has complied with the World Bank’s lending and financial analysis criteria and therefore validates it in the eyes of commercial banks.

7. Bonds

Bond financings are similar to a commercial loan structure, except that the lenders are investors purchasing the borrower’s bonds in a private placement or through the public debt market. The bond holders are represented by a trustee who acts as the agent and representative of the bondholders.

Bonds are generally the most conservative source of financing for a project.

8. Institutional lenders

Institutional lenders include life insurance companies, pension funds, investment funds, mutual funds and charitable foundations. These entities can be a major source of funding.

9. Sponsors

Sometimes, there is no other way to fund the project other than through a direct loan or advance by a sponsor. Such direct loans may also be necessary consequential to cost over-runs or other contingent liabilities that the sponsor has assumed.

10. Host government

The host government can also be a direct or indirect source of financing. The government can loan funds to the project company. As an indirect source, the government may provide tax relief, tax holidays and waiving duties for project equipment, among other freebies.

The participation of a host government comes with a plethora of advantages.

These include reducing the impact of leverage, subordination and foreign exchange burden on the project sponsors.

Government support also decreases political risk, which can assist in attracting private capital.

Conclusion

The bulk of the debt capital for infrastructure projects is provided by national and foreign commercial banks and other financial institutions.

Usually, two or more banks and financial institutions provide a loan to a borrower known as a syndicated loan. International and regional financial institutions like the World Bank also provide loans, guarantees or equity to privately financed infrastructure projects.

Institutional investors like investment funds, insurance companies, mutual funds and pension funds usually have substantial sums available for long term investment and represent an important source of financing either through private placement or via bond purchases.

Jacob Mutevedzi is a commercial lawyer and commercial arbitration practitioner contactable on [email protected], on Twitter @jmutevedzi_ADR and on +263775987784. He writes in his personal capacity.