eBusiness Weekly

Kudzanai Sharara Taking Stock

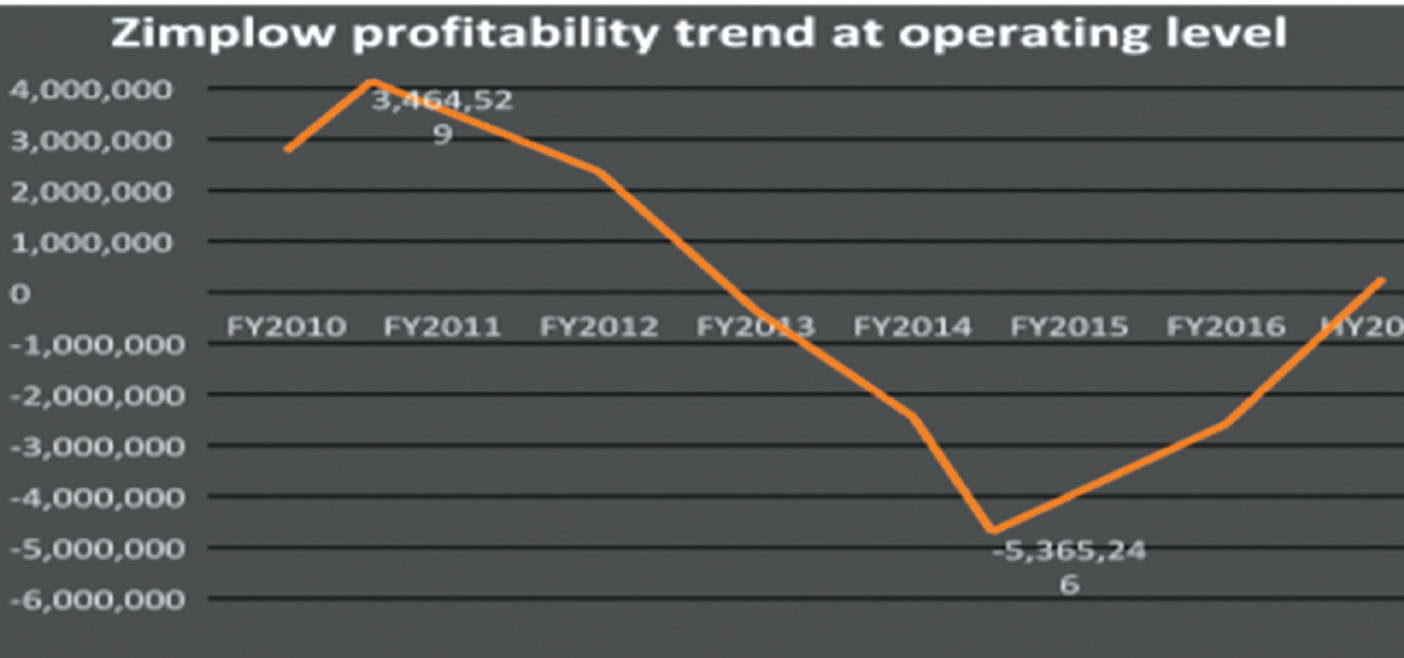

Zimplow’s results for the half year ended June 30, 2017 were not good. But they were encouraging. For a company that had been recording losses since 2012, any change in fortune, no matter how small, is heartening.

However, calling the return to profitability in the first half a recovery would be a fervid leap of the imagination. A $278 931 after tax profit for period is not something to celebrate for a listed entity. But it gives you hope. When you do a trend analysis and realise that the losses were as high as $5,3 million in 2015 then you begin to appreciate that it took a lot of hard work and leadership to stop the haemorrhage.

But how did the wheels come off in the first place?

As promised last week, this will be a regular feature in this publication. The aim is to Take Stock of where we have been and where we are going.

Wrong turn or lack of clear-cut strategy?

It started with the acquisition of Tractive Power Holdings (TPH), a business that was meant to strengthen and bring diversity to Zimplow’s one dimensional product offering — animal drawn implements. With its tractors and other heavy farming implements, TPH was meant to modernise Zimplow’s old aged business model.

It looked like a brilliant tie up but a poor rainfall season that followed made the deal like one made in hell. The company, which had been profitable all along recorded a loss.

Apart from a poor rainfall season in the 2012/13 season, the fall in revenues and the resultant loss is also on account of a poor strategic plan to integrate the old business and the new acquisition. The cost structure was too high and there were a lot of duplications.

But how significant was the failure to tie up the two entities?

While the acquisition of TPH in 2012 was expected to strengthen Zimplow’s earnings potential as well as help diversify the company’s income streams, it came with its baggage including debts of approximately $6 million.

The new acquisition also came with restructuring costs of $1,9 million plus a high cost of interest amounting to $1 million, automatically sending the company’s earnings into the negative territory, for the first time since the adoption of the multi-currency system as shown by the table below.

Questions would then be asked, was the acquisition of TPH by Zimplow right?

I believe it was right then, and still makes a compelling investment case. What was lacking then, was a clear cut strategy. So many things were overlooked. Nobody really thought about the cost side, about the best fit for the business.

Zimplow restructured its operations into four clusters, namely mining, agriculture, property and motoring.

But with revenues falling and both the agricultural sector and mining sector struggling, the structure soon became a burden too heavy to be carried.

Management was also not decisive. When they needed serious surgery to the business, they did it piecemeal with the sale of Puzey and Payne the only notable decision. Losses continued unabated and shareholders changed.

A new chairperson was appointed, followed by a change in the company’s executive, with CEO/MD Zondi Kumwenda leaving.

Enter Thomas Chataika

The new chairman and the new executive immediately embarked on integrating the two businesses. Operations were streamlined to remove duplication of roles and processes among operating units.

Speaking in an interview with Business Weekly this week, a member of the new executive, financial director Vimbai Nyakudya said on taking over, they soon realized that the merger between TPH and Zimplow had not been fully optimised.

Restructuring key to sustainable turn around

“We thus embarked on a restructuring exercise that saw us reducing the head count and centralising certain functions. The exercise yielded a lot in terms of cost containment. It was a long time coming, but we can now see the fruits.

“We also worked on improving productivity, changing the culture and mindset of our employees,” said Nyakudya.

Like a carrot and stick, the Zimplow management increased employee supervision but also put in place appropriate incentives that rewarded attaining set targets.

“As a result we beat record production in the month of August.”

Command agriculture to the rescue?

There is no denying that increased government spending through command agriculture coupled with a good rainfall season has propped up Zimplow’s revenue growth.

Nyakudya acknowledges that but explains: “Yes we have to acknowledge that revenues were boosted by a good agricultural season and firm producer prices, but this would have still come to naught had we not taken the initiative to cut costs and increase productivity.

“We had to make sure that there were no gaps in the supply of our products and with the help of the RBZ’s support in accessing foreign currency our products were readily available to take advantage of the increased demand,” he said.

Nyakudya said demand for Zimplow’s products was not only on the local front but also in the region resulting in export proceeds increasing to $2,1 million from $0,1 million prior year comparative.

“In the last couple of years our products have not been competitive on the regional market given the strength of the US dollar against regional currencies. But in the first half of the year there was some sort of stabilisation on comparative pricing with the bulk of the sales being recorded in Angola.

“We made sales in Zambia, Malawi and Botswana, but Angola was the major driver,” Nyakudya said. In the outlook, he pointed out the Company was confident that the first half’s performance will be surpassed.

Judging by the first half it’s hard not to notice that Zimplow has a compelling growth story as it stands to benefit from mining and agriculture, the two sectors anticipated to spearhead economic growth.

“There are already indications that Government’s support will be very strong in the coming season, through command agriculture.

And what’s happening in other business units?

The mining sector is touted as one of the country’s economic pillars and it should be Zimplow’s major source of business.

“We are also looking at making improved sales in the mining sector, with coal mining company Hwange looking at increasing open cast mining which requires some of our products,” said Nyakudya adding that gold miners will also weigh in positively given the support to machanise the sector that is being spearheaded by the Government and the RBZ.

Is Mealie Brand modern in enough for sustained demand?

At some point questions were raised that the Mealie Brand business model was now outdated as farming was becoming more mechanised. Nyakudya, however, believes that the demographics in the country and those in the region still has a few more years with animal drawn implements.

“There is still a lot of subsistence farming taking place in Zimbabwe and in the region, so animal drawn implements are still on demand.”

I agree. With most farmers still finding it hard to access funding, animal drawn implements is the most viable option for years to come.

There’s a silver lining, but. . .

The silver lining is that the company managed to stop the bleeding but are we going to have a decent bounce off the bottom?

With much of the cost cutting measures having been implemented, much will depend on how much of sales the company would record.

A good agricultural season will be key, and with the Government keen on supporting agriculture and ramping up production in the mining sector, nothing is impossible.